PM-Vidyalaxmi Scheme 2026: How Students Can Get Collateral-Free Loans for Higher Education

Higher education has become one of the biggest investments for Indian families. Whether a student dreams of becoming an engineer, doctor, lawyer, researcher, or management professional, or pursuing specialized courses in India or abroad, the rising cost of education often becomes a major challenge. Tuition fees, hostel charges, books, exam costs, travel expenses, and other educational requirements can create a financial burden that prevents talented students from pursuing their ambitions.

To address this issue and make education more accessible, the Government of India has introduced several student-friendly financial support initiatives over the years. One such important initiative is the PM-Vidyalaxmi Scheme, which helps deserving students access education loans with simplified procedures. A key attraction for many applicants is the availability of collateral-free loans, which removes the need for families to pledge property or other assets to secure educational funding.

In 2026, students and parents continue to show strong interest in understanding how this scheme works, who can apply, what benefits are available, and how to successfully obtain a loan. This guide explains everything in simple language.

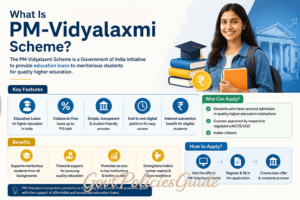

What Is the PM-Vidyalaxmi Scheme?

The PM-Vidyalaxmi Scheme is an education financing initiative designed to help students access loans for higher education through a streamlined and student-friendly process. The scheme aims to reduce financial barriers and encourage deserving students to continue their academic journey without interruption.

The initiative is closely associated with the education loan framework available through participating banks and financial institutions. Instead of approaching multiple lenders individually, students can benefit from a more organized loan application process.

The scheme focuses on:

- Improving access to higher education financing

- Supporting meritorious students

- Reducing dependency on private high-interest borrowing

- Encouraging financially weaker families to support children’s education

- Promoting transparency in loan processing

One of the most attractive aspects is the availability of collateral-free funding under eligible loan categories.

Why the PM-Vidyalaxmi Scheme Matters in 2026

Education costs have increased significantly in recent years. Professional and technical courses often require lakhs of rupees, making self-funding difficult for middle-class and lower-income families.

Common educational expenses include:

- Tuition fees

- Admission charges

- Hostel accommodation

- Library deposits

- Books and study materials

- Laboratory fees

- Examination fees

- Laptop or equipment expenses

- Travel expenses

- Insurance where applicable

For many families, paying these costs upfront is unrealistic.

The PM-Vidyalaxmi Scheme helps bridge this gap by making structured financing accessible.

Its importance in 2026 includes:

Financial Inclusion

Students from modest backgrounds can pursue quality education.

No Immediate Financial Pressure

Families do not need to arrange the full amount immediately.

Collateral-Free Support

Eligible students may avoid pledging assets.

Better Academic Opportunities

Students can choose stronger institutions instead of compromising due to budget constraints.

Lower Dependence on Informal Borrowing

Private borrowing often comes with high interest and financial stress.

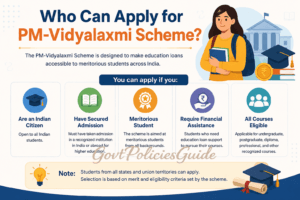

Who Can Apply for the PM-Vidyalaxmi Scheme?

Eligibility may vary depending on the participating lender and specific loan product, but common conditions include:

Indian Citizenship

Applicants generally must be Indian citizens.

Admission to Recognized Institution

The student should have secured admission to an approved educational institution.

Eligible institutions may include:

- Universities

- Engineering colleges

- Medical colleges

- Management institutes

- Professional training institutions

- Government-recognized higher education institutions

Approved Courses

Courses usually include:

- Undergraduate programs

- Postgraduate programs

- Professional degree courses

- Technical education

- Vocational programs

- Specialized academic programs

Academic Merit

Some cases may require merit-based admission.

Co-Applicant Requirement

A parent, guardian, or spouse may need to act as co-borrower.

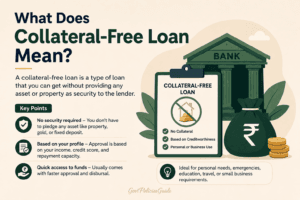

What Does Collateral-Free Loan Mean?

Collateral refers to an asset pledged as security against a loan.

Examples include:

- House property

- Land

- Fixed deposits

- Financial securities

A collateral-free education loan means students can borrow within eligible limits without offering these assets as security.

This is especially beneficial because many families may not own sufficient assets.

Advantages include:

- Faster processing

- Reduced documentation burden

- Lower stress for parents

- Better access for first-generation learners

- More inclusive educational financing

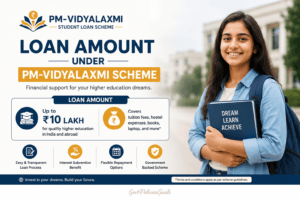

Loan Amount Under PM-Vidyalaxmi Scheme

Loan limits may vary depending on:

- Course type

- Institution category

- Lender policy

- Student eligibility

- Domestic vs overseas study

Common education loan structures may support funding for:

Smaller Loan Requirements

For short-term or lower-cost courses.

Medium Loan Requirements

For undergraduate and postgraduate programs.

Higher Loan Requirements

For expensive professional or overseas education.

Students should confirm exact limits with the lending institution at the time of application.

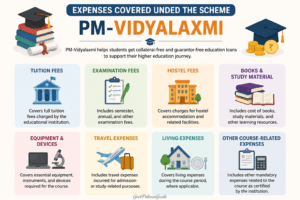

Expenses Covered Under the Scheme

Education loans under this framework may cover:

Tuition Fees

The primary academic fee charged by the institution.

Hostel Charges

Accommodation costs if staying away from home.

Examination Fees

University or institutional exam-related charges.

Library Fees

Applicable institutional usage charges.

Books and Study Material

Textbooks, reference material, and academic resources.

Equipment

Items such as

- Laptop

- Instruments

- Academic tools

Travel Expenses

Especially relevant for overseas programs.

Insurance Premium

Where mandated under loan terms.

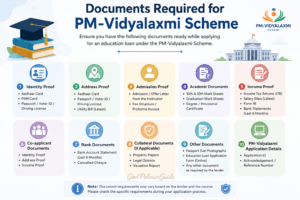

Documents Required

Students should prepare documents in advance.

Common requirements include:

Identity Proof

Examples:

- Aadhaar card

- Passport

- PAN card

Address Proof

Examples:

- Utility bill

- Aadhaar

- Voter ID

Academic Documents

Including:

- Mark sheets

- Passing certificates

- Entrance exam scores

- Admission letter

Fee Structure

Official fee schedule from the institution.

Income Proof

For parent/co-applicant:

- Salary slips

- IT returns

- Bank statements

Passport Photos

Recent photographs.

Bank Statements

As requested.

Course Details

Complete academic information.

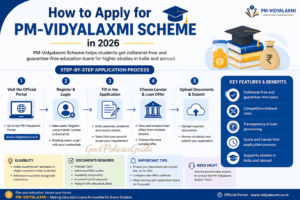

How to Apply for PM-Vidyalaxmi Scheme in 2026

The process is generally straightforward.

Step 1: Gather Academic Information

Keep:

- Admission proof

- Course details

- Fee structure

ready.

Step 2: Prepare Financial Documents

Collect income and identification records.

Step 3: Access Application Platform

Use the designated official application route for education loan processing.

Step 4: Fill Student Details

Provide:

- Name

- Contact details

- Academic background

- Course information

Step 5: Add Co-Applicant Information

Enter parent or guardian details.

Step 6: Upload Documents

Ensure all uploads are clear and complete.

Step 7: Submit Application

Review before final submission.

Step 8: Verification

The lender evaluates:

- Academic eligibility

- Repayment capacity

- Documentation accuracy

Step 9: Loan Approval

Approved applicants receive sanction details.

Step 10: Disbursement

Funds may be released according to institutional payment schedules.

Interest Rates

Interest rates are not always fixed across all lenders.

Rates depend on:

- Bank policy

- Applicant profile

- Course category

- Loan amount

- Risk assessment

Students should compare lenders carefully.

Important considerations:

- Floating vs fixed rates

- Processing charges

- Moratorium terms

- Prepayment rules

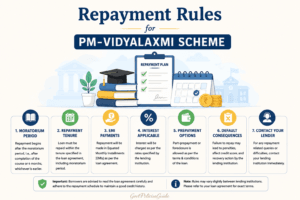

Repayment Rules

Education loans usually offer flexible repayment structures.

Moratorium Period

Repayment may begin after:

- Course completion

- Additional grace period

This helps students settle into employment first.

EMI Repayment

Monthly installments begin after the moratorium.

Early Repayment

Some lenders permit early closure.

Prepayment Conditions

Check if charges apply.

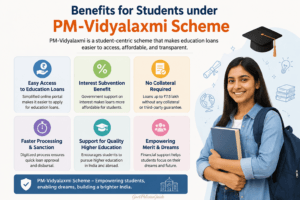

Benefits for Students

No Need to Sell Assets

Families can preserve savings and property.

Better Access to Quality Education

Students can choose stronger institutions.

Reduced Financial Stress

Structured financing creates predictability.

Supports Career Growth

Education becomes an investment rather than an obstacle.

Encourages Equal Opportunity

Students from financially weaker backgrounds benefit significantly.

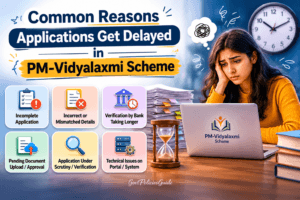

Common Reasons Applications Get Delayed

Many applications slow down because of preventable mistakes.

Incomplete Documentation

Missing records cause delays.

Incorrect Information

Mismatched details create verification problems.

Weak Academic Documentation

Incomplete academic history may affect assessment.

Admission Not Finalized

Conditional admission can complicate approval.

Poor Co-Applicant Financial Profile

Repayment concerns may impact processing.

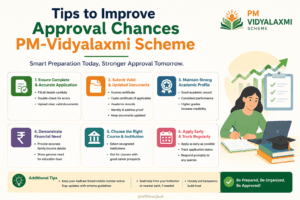

Tips to Improve Approval Chances

Apply Early

Do not wait until fee deadlines.

Keep Documents Organized

Use scanned copies in clear format.

Verify All Information

Double-check spelling and figures.

Understand Loan Terms

Know interest and repayment conditions.

Maintain Communication

Respond quickly to lender requests.

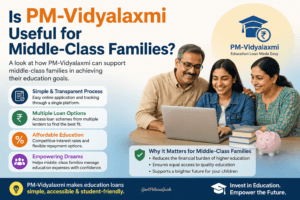

Is PM-Vidyalaxmi Useful for Middle-Class Families?

Yes, absolutely.

Middle-class families often face a difficult gap:

- Income may be too high for some scholarship categories

- Savings may still be insufficient for expensive education

The scheme helps address this issue by making financing structured and accessible.

This can be particularly useful for:

- Engineering aspirants

- Medical students

- MBA applicants

- Law students

- Students pursuing overseas education

- Specialized professional learners

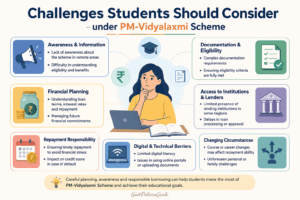

Challenges Students Should Consider

Even good financing requires responsibility.

Potential concerns include:

Debt Responsibility

Loans must be repaid.

Interest Accumulation

Longer repayment increases total cost.

Employment Uncertainty

Repayment depends on future income.

Documentation Burden

Applications require preparation.

Students should borrow realistically.

PM-Vidyalaxmi vs Traditional Borrowing

| Feature | PM-Vidyalaxmi Route | Informal Borrowing |

|---|---|---|

| Structured Process | Yes | No |

| Transparent Terms | Yes | Often unclear |

| Education-Focused | Yes | No |

| Potential Moratorium | Yes | Rare |

| Collateral-Free Options | Available | Usually not |

| Consumer Protection | Better | Limited |

The difference can be significant for families.

Frequently Asked Questions

Is collateral mandatory?

Not always. Eligible categories may qualify for collateral-free loans.

Can postgraduate students apply?

Yes, eligible postgraduate students may qualify.

Is parental income important?

Yes, co-applicant financial evaluation may matter.

Can overseas education be funded?

Some education loan structures may support international study.

Is repayment immediate?

Usually not. Moratorium periods are common.

Can self-employed parents be co-applicants?

Yes, subject to lender assessment.

Final Thoughts

Higher education should be driven by talent and ambition—not limited by immediate financial constraints.

The PM-Vidyalaxmi Scheme offers an important pathway for students who need education funding, especially those seeking collateral-free loan options. By simplifying access to financing and reducing the burden of upfront payment, the scheme can make quality education more attainable for thousands of families.

However, education loans are financial commitments, not free assistance. Students should understand terms carefully, borrow only what they genuinely need, and plan repayment responsibly.

For ambitious students in 2026, this scheme could be a practical stepping stone toward academic and career success.